Introduction

In support of our FinNeeds research, insight2impact recently undertook a study in Nigeria. This project piloted an innovative research method that combines traditional demand-side research instruments, in the form of face-to-face surveys, with transactional data generated by the Nigeria Central Switch’s inter-bank settlement system (Nigeria Inter-bank Settlement System or NIBSS). Our goal was to better understand the digital financial services landscape, how it currently serves the people of Nigeria and how it can be improved to better serve their FinNeeds.

Methodology

Our analysis of transactional data generated by NIBSS leverages Nigeria’s Bank Verification Number (BVN), a unique customer identifier reported together with bank account details for every transaction processed by NIBSS. Because NIBSS processes several billion transactions for over 36.5 million BVNs each year, the analysis was conducted on a randomly drawn sample of one million BVNs. A full transaction history covering various payment platforms supported by NIBSS and ending in December 2017 was extracted for each of these BVNs. These transaction histories include point-of-sale (POS), NIBSS electronic funds transfers, cheque payments and instant payments. Because NIBSS is a switch, only inter-bank transactions are processed through its platforms; and no balances, data on cash withdrawals or transactions between clients of the same bank are visible. Aside from the available transaction data, customers provide some basic demographic data during the BVN registration process: age, gender, contact details and location at the time of registration.

In addition to transactional data, the project team analysed demand-side survey data collected by insight2impact during November and December 2018. A sample of 1,339 adults were interviewed in urban centres in Lagos and 1,058 in Kano states. Along with various demographic and contextual indicators, the survey explored payment use cases to assess the adoption of digital payment solutions. A further 611 respondents selected from the NIBSS sample were also interviewed. For these respondents, survey data that provides rich context as well as useful reported payments behaviour (together with a sub-set of actual payments data generated by NIBSS) is available, although the data is not contemporaneous – transactional data terminates at the end of 2017, while the survey data was collected at the end of 2018. We were also able to populate nationally representative indicators by drawing on the 2018 EFInA Access to Finance survey.

Key findings

Digital receipts

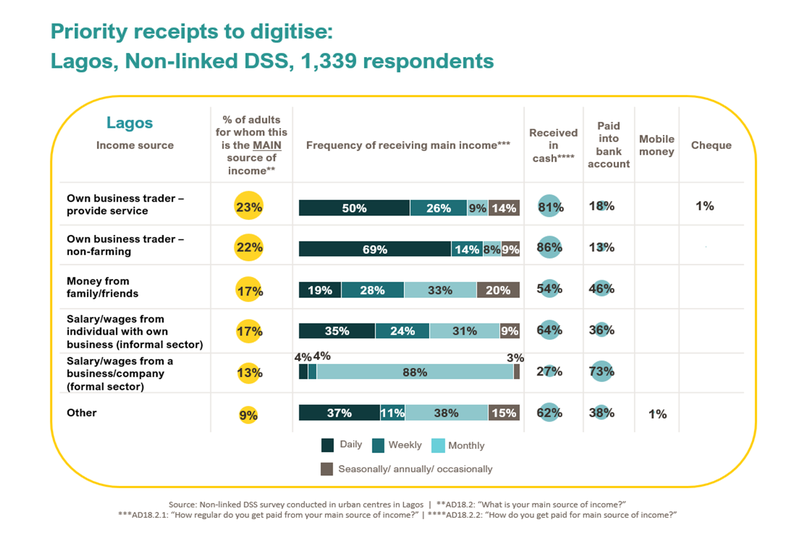

In line with other data, the demand-side survey found relatively low adoption of digital solutions for either receiving income or making payments. Of those who report receiving some income, including remittances, 35% in Lagos and 17% in Kano reported receiving some of this income directly into an account. Unsurprisingly, formal salaries and government-to-person payments are mostly digitised. While there is some scope to digitise these payments further, to drive digital adoption meaningfully across the Nigerian economy, other income streams will need to be digitised – notably small business owners and other merchants. Exhibit 1 illustrates the income sources in Lagos that are priorities for digitisation.

Exhibit 1

Those who receive their main source of income digitally are significantly more likely to have made at least one fully digital payment1 in the past 90 days than those who receive their income in cash. Perhaps noteworthy are the people who receive their income entirely in cash but have access to an account or digital store of value. Of these people, 28% of customers in Lagos and 17% in Kano go on to make at least one fully digital payment.

The analysis of the drivers of digital payments supports the finding that receiving a digital receipt is the biggest predictor of whether or not a person will make a fully digital payment.

Digital payments

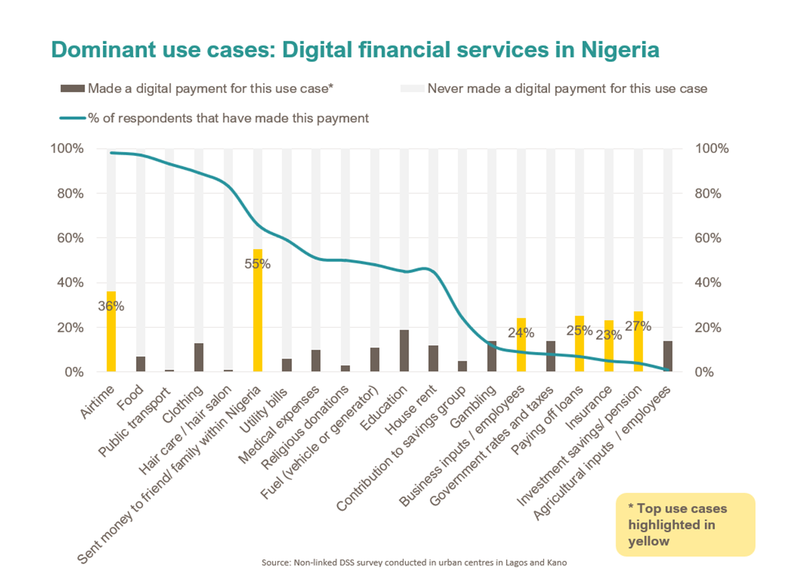

Adoption of digital payments differs significantly by use case. Sending remittances and airtime purchases are most likely to have been initiated via a digital channel. There is clearly scope for increased digitisation of these payments. On the other hand, food, clothing, haircare, medical expenses and education are almost always paid for in cash. Encouraging merchants to accept digital payments is clearly a challenge. Half the respondents in Lagos and almost two-thirds in Kano indicate that merchants in their areas do not accept digital payments. Of course, this may, in part, reflect merchant perceptions of customer willingness to pay digitally, a “chicken and egg” circular dependency inherent in payment innovation. Exhibit 2 illustrates the current dominant use cases for digital payments in Nigeria. The graph shows the percentage of respondents who have made a particular payment, along with those who made the payment by using a digital channel. Of the use cases explored in this study, the most common digital payments were to purchase airtime and to send money to a friend or family member within Nigeria. The high occurrence of, but low percentage of digital payments for, purchasing food, clothing, haircare and paying for public transport clearly show high priority areas for digitisation.

Exhibit 2

NIBBS instant payment system vs POS

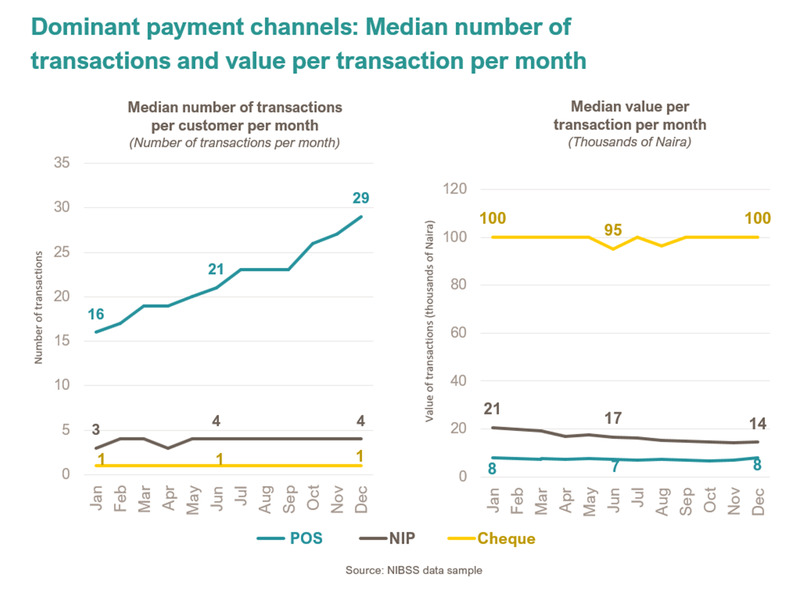

Overwhelmingly, digital payments are being made via mobile channels, principally USSD as opposed to POS or ATMs. Many are inter-bank credit transactions made using NIBSS’s innovative instant payment platform (known as NIP). This platform was introduced in 2011 and is the only solution of its kind on the continent. Its impact is clear, particularly relative to other digital channels, notably POS. While there has been a noticeable increase in the number and value of POS transactions, as well as the deployment of POS terminals, this is dwarfed by the growth in NIP transactions. This highlights the importance of a well-priced, instant payments solution that mimics the immediacy and convenience of cash to drive digital payments.

While the analysis of transaction volumes and values is impressive, the analysis at a customer level demonstrates just how transformative NIP has been. Within the sample of customers analysed as part of this project, there are roughly three times as many NIP transactions as POS transactions, but there are over 10 times as many customers who transact over NIP. While the growth in the number of POS transactions appears to be driven by an increase in the number of transactions per customer, the growth in number and value of NIP transactions has been driven by transactions from new customers. Despite the growth in deployment of terminals, the number of POS customers who transact each month has remained stable.

Exhibit 3

POS customers transact more frequently and are more likely to have transacted within the last month. The median transaction value for POS payments remained stable in 2017, whereas the median values of NIP transactions are declining. On that platform, customers who are first visible in the sample more recently have lower-average transaction values than customers who are visible earlier on – an observation that is consistent with increased inclusion. This data shows that the NIP platform is able to serve lower-income customers – a challenge that most other platforms are struggling to overcome. Exhibit 3 compares the median volume and value of transaction across POS, NIP and Cheque transactions.

Customer profiles

Transactional data was used to segment NIBSS customers along two primary dimensions: volume and value of transactions across all platforms. The segmentation clearly identifies a large segment of users who transact infrequently. While this is of course a partial picture that misses many intrabank transactions, notably airtime purchases, it does reflect the very limited usage of digital payments across use cases as per the demand-side survey.

As noted, the NIBSS data provides limited demographic data. To understand the customer more holistically and to generate a more complete understanding of their interaction with digital payments, a demand-side survey was conducted with 661 respondents who could be linked to the NIBSS. While one of the original objectives of this research was to compare usage data recalled by survey respondents with actual transactions, this comparison did not yield conclusive findings.

Exhibit 4

![]()

Nevertheless, the matched sample is a useful addition, which helps to reveal customer personas for each segment and explore his or her experiences of, and attitudes to, the transaction platforms and channels that NIBSS enables. This is in itself a valuable exercise that can build a customer-centric approach within NIBSS and its shareholder banks. Exhibit 4 is one example of the personas developed, particularly that of “Mrs Damilola”, one of NIBSS’s high-frequency transactors.

Taking the next steps

This analysis is a pioneering piece of work that places the customer at the centre of the analysis. While many questions remain unanswered, it has enabled an understanding of the potential of NIBSS’s data to explore behaviour. It also provides a basis to develop reporting outputs that use the customer, rather than volume or value of transactions, as the primary unit of analysis.

Transactional data can support an evidence-led strategy to drive digital adoption specifically in poorer areas of the country and to assess the impact of specific interventions that may be implemented. With regard to receiving income, survey data indicates there is some scope to increase government-to-person payments and payment of salaries in the formal sector. Likewise, with regard to making payments, digitising all person-to-government payments (including payment for utilities) is a clear first step.

In light of the relatively low incidence of these payments, for Nigeria to see broad adoption of digital payments it must find ways to encourage merchants to accept, and consumers to adopt, digital payments across a range of payment use cases. This is a significant challenge, absent compulsion. While it is possible that in some value chains an adoption strategy can leverage the power of aggregators and financial providers (specifically in credit), if digital payments are to be adopted widely and willingly, the digital payments proposition must be better than cash. The NIP platform that enables instant transfer of value at low cost, together with mobile channels that enable anywhere, anytime transactions have laid the foundations. But there are still clear gaps. One is the limited number of cash-out facilities that would enable convenient conversion between digital and hard currencies. If cash is hard to come by, users will be wary of forgoing it, particularly if digital payments are not universally accepted.

The Shared Agent Network Expansion Facilities (SANEF) strategy, which will deploy half a million agents across Nigeria, can close this gap. But it is critical that this deployment be guided by good evidence and be closely monitored by using transactional data aggregated at both agent and customer levels. Given that NIBSS will be the switch that enables interoperability within this network, the data it generates will be critical.

Of course, NIBSS data is not sufficient on its own to monitor adoption of digital payments solutions. As noted, it cannot provide visibility on intrabank transactions, which are likely significant in an agent-driven model. It is therefore critical that the analysis described in this report be used to crowd in key partner banks and other switches that will play a significant role in facilitating digital payments in Nigeria.

Conclusion

In addition to profiling customers, the richness of transactional data can, inter alia, enable an analysis of digital payment journeys by exploring how those who receive income into an account subsequently transact, for example the adoption journeys of young, first-time account holders. It can also enable a better understanding of networks and linkages between customers, a potentially important area for further investigation given that word-of-mouth is likely to be effective in encouraging new users to adopt payment solutions. In addition, it can support the agent strategy directly.

Aside from generating useful findings, the project has demonstrated that an analysis of transactional data is possible without compromising data security or customer privacy. This should put to rest many of the justified concerns of individual banks. NIBSS could consider working with the Central Bank of Nigeria to develop and publish clear protocols regarding how transactional data is analysed and how customer data is anonymised. It should also ensure that appropriate disclosure on data usage and clearly worded consent agreements be included when customers sign up for BVNs or bank/mobile money accounts.

This exploratory analysis, useful in and of itself, clearly demonstrates the potential power of transactional data. Furthermore, the extremely valuable transaction analysis would not have been possible without the existence of the BVN – a national asset that places Nigeria well ahead of many other nations. Maintaining and updating the BVN database should be a high priority, as the richness and completeness of the data facilitated by the BVN create a unique data context that supports an entirely new approach to the measurement of financial inclusion. Within NIBSS itself, further analysis can explore merchant payments, customer adoption journeys over time and network efforts. Because the BVN is a unique country-wide identifier, further iterations of analysis could potentially merge masked data from other switches with NIBSS data to incorporate ATM transactions, as well as masked data from banks and MNOs to capture “on-us”’ payments as well. This research project has only scratched the surface of what is possible with transaction data.

Wondering how to find us? Get involved and contact us isabelle@i2ifacility.org.

________________________________________________________________________________________________________________________

1A fully digital payment is one where the store of value is digital and the payment instruction is issued over a digital channel, i.e. no cash is involved in the transaction. Digital channels include mobile phones, the internet, POS devices and ATMs.