Financial services can help individuals to manage their money, plan for risks, start entrepreneurial ventures and build assets over time. These benefits are, however, not guaranteed; and unintended behaviour such as over-indebtedness, late credit repayment or defaults, insurance lapses or dormant accounts can erode the value that clients derive from them.

To assist financial service providers in understanding how their product design, pricing and customer communication influence customer uptake and usage behaviour, we have undertaken two systematic reviews of publicly available evidence. These systematic reviews sought to identify behavioural interventions that have been proven to influence a credit, saving, insurance or payment decision.

We’ve published the results from the first systematic review here, and we’ve captured and categorised (in our interactive online database) the papers identified in the first and second review. This blog will highlight the key insights from our update to the initial review.

Our second review identified 53 additional studies that have become publicly available since our review in 2017. This increases the number of studies that capture the relationship between a behavioural intervention and a financial decision from 97 to 150. The additional studies have significantly expanded the geographic coverage, diversity of contributing authors and the behavioural interventions that have been tested on financial services.

The second review has added 12 additional countries, which include Burkina Faso, Brazil, Germany and Senegal. This increases the total number of countries in our database to 42. The majority of the studies have been conducted within the United States, followed closely by India and the Philippines.

The total number of authors that have contributed to this field has increased from 186 to 311. Some new authors to our database include Merve Akbas, Syon P. Bhanot, Eric Johnson, Lauren Eden Jones and Tatiana Homonoff. The top three contributing authors, by number of studies conducted overall, are Dean Karlan, Hal Hershfield and Dean Yang.

Additional behavioural interventions: new findings

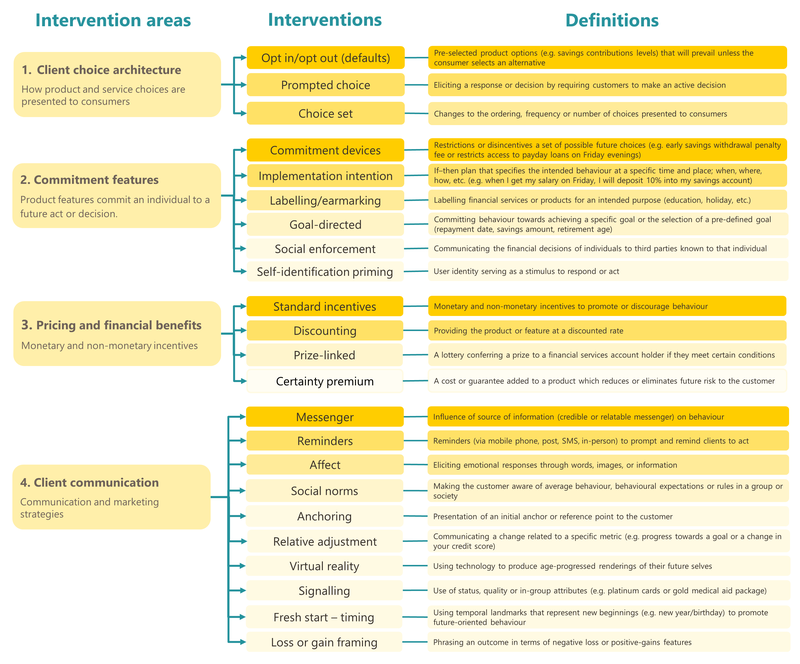

A key finding from this update has been the addition of five new behavioural interventions (highlighted in Figure 1) that have been publicly tested within financial services for the first time, increasing our framework to include a total of 23 behavioural interventions.

Figure 1: Behavioural interventions

The five new behavioural interventions identified have been applied across client choice architecture, pricing and financial benefits, and client communication. A full explanation of the first 18 interventions can be found in the focus note Behavioural interventions that advance financial inclusion. Below, we provide an overview of the new interventions identified.

Choice set interventions related to any changes to the ordering, frequency or number of choices presented to new or existing consumers.

The manner in which product and service choices are presented to consumers has been shown to play an important role in influencing customer purchasing decisions. A study in the United States varied the options offered to customers in terms of the level of granularity provided to consumers; some individuals were given the option to make deposits daily and the others monthly (Hershfield, Shu & Benartzi, 2018). These changes in the choice set increased the take-up of a savings account four-fold.

Certainty premium intervention is a cost or guarantee that’s added to a product to reduce or eliminate future risk to the customer.

This intervention was tested in an experiment in Germany where different groups of individuals were exposed to varying levels of default risk within their insurance contracts (Zimmer et al., 2018). These levels ranged from 0% (a risk-free insurance contract) to 3% default risk. This study found that participants’ willingness to pay decreased from €54 for the risk-free contract to €29 for the contract with 3% risk. Individuals are therefore willing to pay a significantly higher premium to ensure greater certainty in their insurance products.

Fresh-start timing interventions use temporal landmarks that represent new beginnings (e.g. first day of the week, month, New Year or birthday) to promote future-oriented behaviour.

These interventions can be effective at changing the customer’s mindset to “turning over a new leaf” and alter their behaviour upon reaching this fresh-start date. A study in the United States looked at whether communicating temporal landmarks – such as one’s birthday or various holidays – would lead individuals to increase their pension contributions (Beshears et al., 2016). They found that the birthday fresh-start option was the most successful at getting people to save more, resulting in a 22-point increase in average contribution rates as a portion of one’s salary. Interestingly, none of the holiday fresh starts – such as New Years and Thanksgiving – were found to significantly influence retirement savings decisions.

Signalling interventions make use of status, quality or in-group attributes when communicating with customers.

Our database captures two types of signalling: quality signalling and status signalling. The first type provided participants in the United States with marketing information on a gold insurance product with the same underlying features as a regular bronze product (Ubel, Comeford & Johnson, 2015). This signalled to the potential buyer, inaccurately, that the gold insurance product was a superior product and hence induced customers to take up the product, regardless of the benefits and services included in the package.

The second type of signalled quality was where gold-credit-card holders in Indonesia were given the opportunity to upgrade to a platinum credit card, but with the same benefits and features of their current gold card (Bursztyn et al., 2017). The demand for the card itself was 21%, which was significantly higher than demand for the associated benefits, which was 14%. New platinum-card holders were also more likely to use their card in social situations, signalling to others their elite social status. In both instances, a superior and preferable option was being signalled, either to or by the consumer.

Relative adjustment: Interventions communicate changes in a specific metric, such as progress towards a goal, or they communicate a change in an individual’s credit score.

In the United States, an experiment measured the effect of communicating information through receipts after consumers had made a purchase (Poddar, Ellis & Ozcan, 2015). The information consisted of the amount of debt accumulated and the individual’s monthly spending. This resulted in experiment participants spending significantly less (9.6%) than a control group. Constant updates to customers on changes in their debt and spending patterns are therefore a useful tool to encourage customers to decrease their overall spending.

Another noteworthy change to our typology of interventions…

We amended the SMS-reminders intervention to focus on reminders in general. Thanks to studies by Fajnzylber and Reyes (2011) and Loibl et al. (2018), we can now track and report on the relative effectiveness of various reminder channels such as postal letters and phone call reminders respectively.

What is next?

To take these insights into action, insight2impact is teaming up with Irrational Labs to undertake a behavioural science training academy with financial service providers in Cape Town, South Africa. Our aim is to empower financial service providers to improve the value of their products to customers through the effective use of behavioural interventions in product design, distribution and client communication. If you’re a financial service provider and would like to join our academy, please reach out to chernay@i2ifacility.org.